How well can Canadians balance mortgage and income : Buying a house today is not easy for Canadians as the real estate prices are soaring sky high calling for more mortgage as the income aggravates at a relatively lower rate.

Gross debt service ratio(GDS) is a proven method used by individuals in Canada to learn about their eligibility and capability for getting mortgage rates. GDS is a percentage of the outlays related to house buying like mortgage interest, principal, taxes and gross annual income. Mortgage payment calculator is also helpful in calculating it.

The ideal percentage for hassle-free mortgage application capped at less than 35.

Today we aim to provide assistance to single income professionals across Canada to assess and find an ideal place where they can afford to live without any financial burden despite of their mortgage.

According to a study conducted by Point2 Homes. The average earning of a professional in Canada is around $50000 a year.

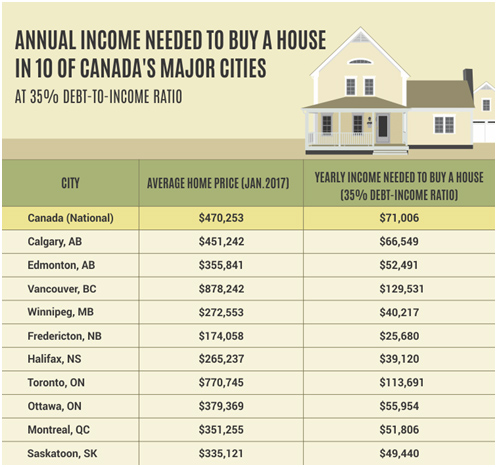

They have also conducted a research to derive the average house cost of houses in popular cities and year income needed as per GDS for mortgage affordability calculator without any encumbrance.

For example, according to the below picture to buy a house in Toronto. The average annual income that needs to earned by an individual is $113,691.

Fredericton seems to be a popular hub in Canada. For people with low incomes with Toronto manages to top the list.

Basically, in major cities the Canadians need to earn. Anywhere around $ 51806(Minimum yearly income to buy a house-Average i.e. $51806- $50000) to $ 80000 more to comfortably. Afford a mortgage in the locality of their choice.

Comments (0):